Physical climate risk has become one of the most material financial risks for banks, NBFCs, and insurance companies in India. Unlike transition risks that arise from policy changes or new technologies, physical climate risk comes from the direct impacts of a changing climate on assets, operations, and customers. From devastating floods and cyclones to rising temperatures and sea levels, these risks are already affecting loan portfolios, real estate values, insurance claims, and credit quality across the country.

In this guide, we explain what physical climate risk really means, the critical difference between acute and chronic risks, the role of CMIP6 climate models, why spatial resolution is so important, and how financial institutions can turn these challenges into manageable strategies using the right technology.

What Is Physical Climate Risk?

Physical climate risk refers to the potential financial losses and operational disruptions that result from climate-related hazards. These risks are location-specific and can directly damage buildings, infrastructure, and entire supply chains. For financial institutions, physical risk translates into higher defaults, reduced asset values, and increased insurance payouts. Regulators like the Reserve Bank of India (RBI) now expect banks and NBFCs to identify, measure, and manage these risks as part of their core risk management frameworks.

Acute vs Chronic Physical Risks: Understanding the Two Categories

Physical climate risks fall into two main categories. Each requires different data, models, and response strategies.

Acute Physical Risks

These are sudden and event-driven. They include intensified cyclones, floods, heatwaves, wildfires, droughts, and extreme storms. Acute risks cause immediate and severe damage, leading to business interruptions, sharp spikes in insurance claims, and sudden increases in loan defaults. In India, frequent urban flooding in Mumbai and Chennai, along with stronger cyclones on the eastern and western coasts, are clear examples. These events are becoming more frequent and intense, creating short-term financial shocks for lenders and insurers.

Chronic Physical Risks

Chronic risks unfold gradually over decades. They result from long-term shifts such as steadily rising temperatures, sea-level rise, changing rainfall patterns, prolonged droughts, and increasing water scarcity. These risks slowly erode asset values, raise operating costs, and reduce productivity. For example, higher average temperatures increase cooling costs for commercial buildings, while sea-level rise threatens coastal properties and port infrastructure across India.

Distinguishing between acute and chronic risks is essential. Acute risks call for strong stress testing around extreme events, while chronic risks require long-term scenario analysis and adaptation planning.

CMIP6: The Foundation for Reliable Climate Projections

To assess physical risks accurately, financial institutions depend on advanced climate science. The Coupled Model Intercomparison Project Phase 6 (CMIP6)is currently the global gold standard for climate projections. Coordinated by the World Climate Research Programme, CMIP6 brings together the world’s leading climate models.

CMIP6 delivers detailed projections for temperature, precipitation, extreme weather events, and sea-level rise under different future scenarios up to 2100 and beyond. It offers major improvements over previous models with better simulation of ocean-atmosphere interactions and cloud processes. Institutions use CMIP6 data along with NGFS scenarios to run forward-looking assessments that help them understand potential portfolio impacts over short, medium, and long time horizons.

However, working with CMIP6 data is challenging. The volume is enormous, often reaching terabytes across multiple models, scenarios, and time periods. Strong cloud infrastructure and advanced analytical tools are necessary to process this information effectively.

Why Spatial Resolution Matters in Physical Risk Assessment

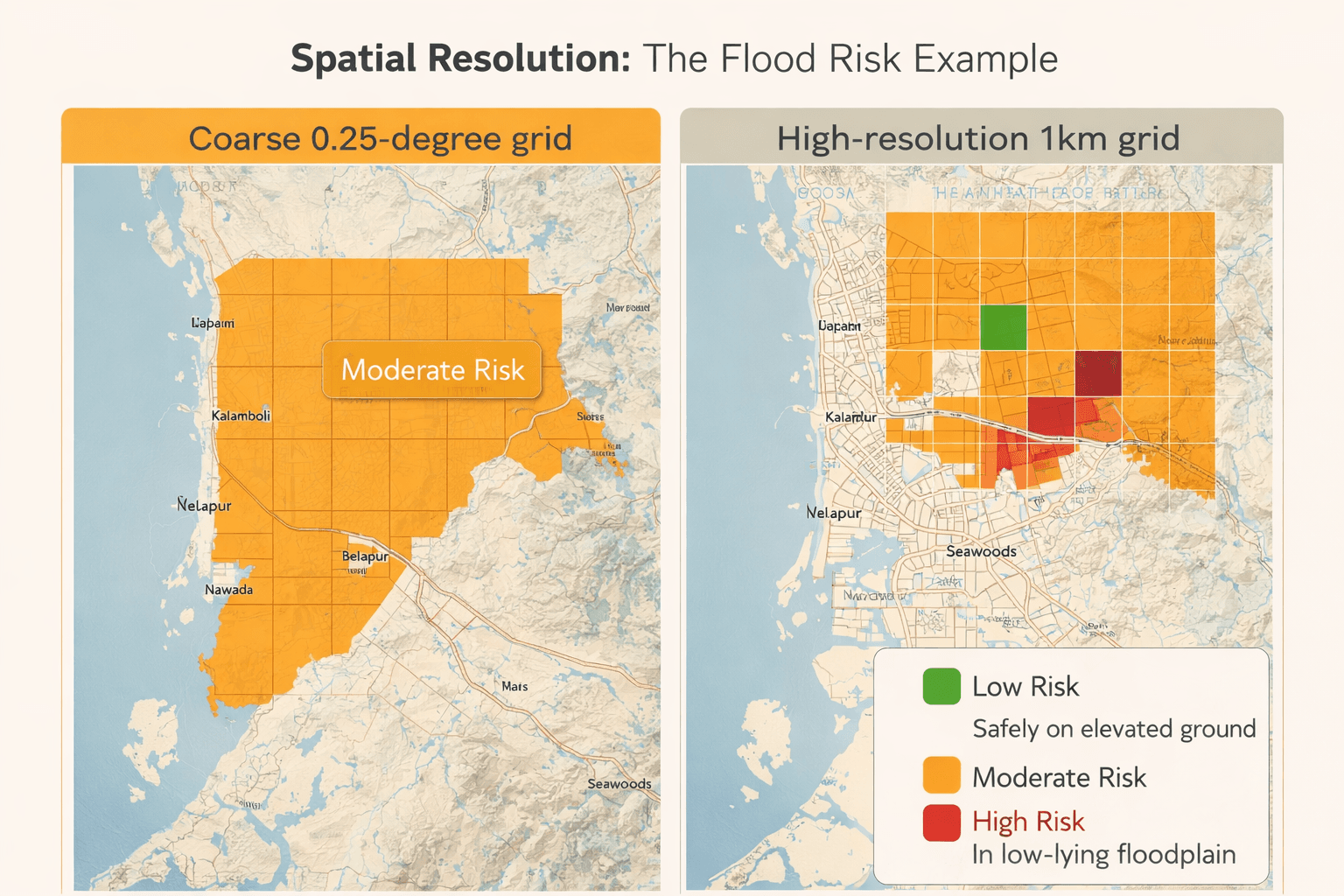

One of the most critical yet often overlooked factors in physical risk analysis is spatial resolution. Resolution refers to the size of the grid cells used in climate and hazard models. It determines how precisely the model can capture local variations in risk.

Coarse resolutions, such as 0.25 degrees (25×25 = 625 sq.km per grid cell), are useful for high-level national or state-wide screening. They help identify broad risk hotspots. However, for accurate decision-making in banking, lending, and insurance, much finer resolution is required.

At coarser levels, the model averages risk across large areas and smooths out important local differences. This can result in inaccurate risk pricing, poor capital allocation, and missed opportunities to identify resilient assets within high-risk zones.

Data Requirements for Effective Physical Risk Assessments

Accurate physical risk modeling begins with precise location data. The minimum requirement is latitude and longitude coordinates for every asset or exposure.

In practice, institutions can begin with:

- One-line addresses

- PIN codes (in India)

- Property records

These inputs are geocoded into accurate lat-long points and then combined with high-resolution hazard layers. Additional valuable data includes asset type, construction details, elevation information, and historical loss records. The quality and precision of this input data directly determine the reliability of the final risk scores.

The Critical Role of Resolution: A Flood Risk Example

Resolution becomes especially important for hazards like flooding. Flood risk depends heavily on micro-level factors such as local elevation, topography, drainage systems, soil type, and proximity to rivers or coastlines.

A 0.25-degree resolution grid may classify an entire district as moderately exposed. In reality, one property may sit safely on higher ground with good drainage, while another just a few kilometers away lies in a low-lying flood plain and faces much higher risk.

For initial portfolio screening, 0.25-degree data serves as a useful starting point. But for regulatory reporting, loan pricing, insurance underwriting, or detailed stress testing, institutions need much finer resolution — often down to 1 kilometer, 100 meters, or even property level. This requires high-quality digital elevation models (DEMs) and local hydrological data.

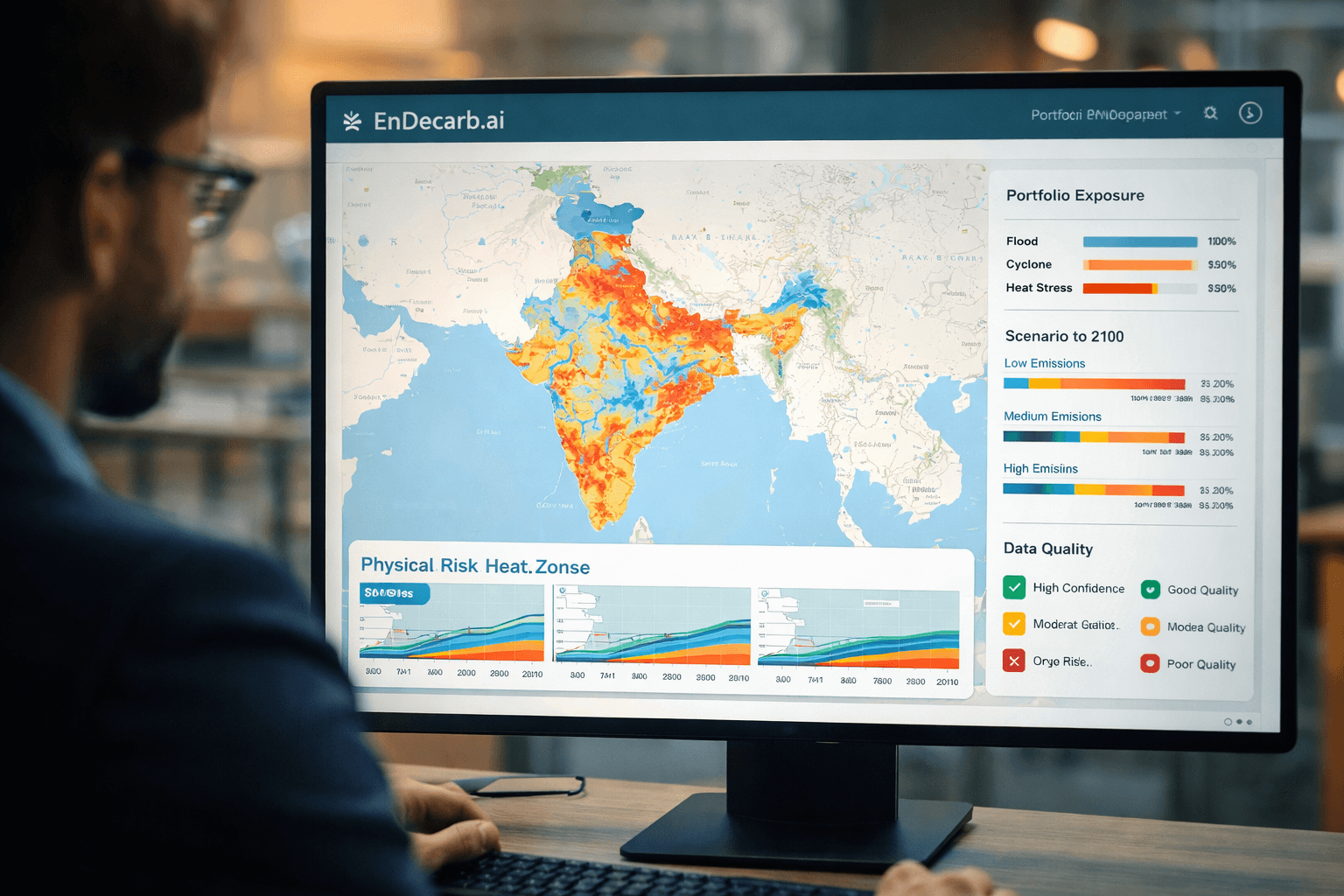

How EnDecarb.ai Provides a Scalable Solution for Physical Climate Risk

At EnDecarb.ai, we have developed a powerful AI-driven climate risk platform specifically designed to help banks, NBFCs, and insurance companies implement robust physical risk assessments at scale.

Our platform efficiently processes large volumes of CMIP6 data and high-resolution hazard layers tailored for Indian conditions. Users can upload portfolios using simple addresses or PIN codes, and the system automatically geocodes (Latitude/Longitude is the gold standard) them for precise analysis. Institutions can begin with broad 0.25-degree overviews and then drill down to finer resolutions where it matters most, such as flood-prone or coastal areas.

Key benefits include:

- Transparent and fully auditable calculations with no black-box models

- Seamless integration of acute and chronic risk metrics

- Portfolio-level stress testing and scenario analysis

- Support for RBI regulatory reporting and internal risk management

- Scalable cloud architecture that grows with your portfolio

Whether you manage thousands of mortgage loans, commercial real estate exposures, or insurance policies, EnDecarb.ai makes sophisticated physical risk analysis practical, accurate, and cost-effective.

Moving Forward with Confidence

Physical climate risk is already affecting financial portfolios across India. By clearly understanding acute and chronic risks, leveraging CMIP6 projections, focusing on proper spatial resolution, and using the right technology, institutions can protect their balance sheets and help clients build greater climate resilience.