For many financial institutions, the biggest climate impact is not inside their own buildings. It is on their balance sheet.

Financed emissions, the greenhouse gas emissions linked to the loans, investments, and underwriting activities of banks, NBFCs, asset managers, and insurers, often dwarf their direct operational emissions by over 100 times. These are the real-world emissions generated by the companies, projects, and customers they choose to finance. Sitting squarely under Scope 3 Category 15 (Investments) of the GHG Protocol, financed emissions have quietly become one of the most material, yet historically under-reported, climate risks in global finance.

What was once considered a niche sustainability topic has rapidly evolved into a core financial and regulatory imperative. In this comprehensive guide, we explore the origins of financed emissions accounting, the globally accepted PCAF framework, the ten key asset classes, the critical importance of data quality, and how forward-looking institutions are turning this challenge into a strategic advantage.

A brief history of financed emissions

Financed emissions grew out of the broader GHG Protocol and Scope 3 accounting movement, which recognized that a financial institution’s climate impact goes far beyond its own buildings and operations (Scope 1 and 2) and extends into the emissions of the companies and projects it finances, its “Scope 3 category 15” or financed emissions. To bring consistency, the Partnership for Carbon Accounting Financials (PCAF) was formed by a group of banks and investors, and in 2020 released the first Global GHG Accounting and Reporting Standard for financed emissions, building directly on the GHG Protocol’s Scope 3 framework. As of early 2026, the Partnership for Carbon Accounting Financials (PCAF) has solidified its position as a leading global standard-setting body for financial institutions, with its 2025 Annual Impact Report highlighting a community of 719 financial institutions representing nearly $100 trillion in total assets across over 85 countries.

Financed Emissions Across Asset Classes

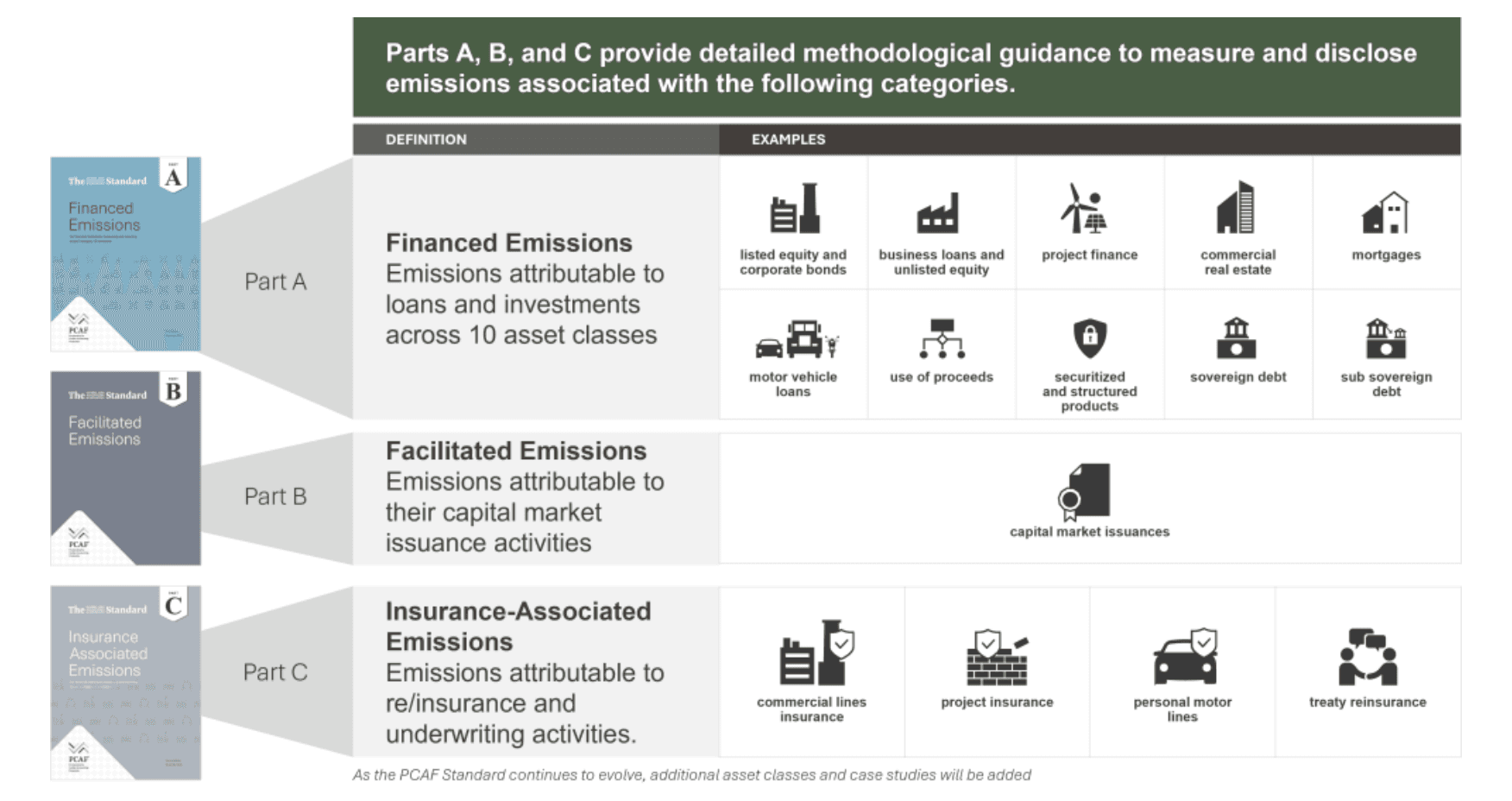

PCAF defines financed emissions methodologies for ten core asset classes in its 2025 standard. On 2nd December 2025, the Partnership for Carbon Accounting Financials (PCAF) launched an updated Global GHG Accounting and Reporting Standard, expanding to ten asset classes.

Before diving into the ten asset classes, it is helpful to understand how the PCAF framework is structured. The Standard is divided into three primary parts that categorize different types of climate impact:

- Part A: Financed Emissions:The core pillar focusing on the GHG emissions associated with a financial institution’s loans and investments (Scope 3, Category 15).

- Part B: Facilitated Emissions:Covers emissions associated with off-balance sheet "capital markets" activities, such as underwriting for equity and debt issuances.

- Part C: Insurance-Associated Emissions: Specifically addresses the emissions linked to (re)insurance underwriting portfolios, helping insurers align their liabilities with net-zero goals.

Each asset class has its own specific calculation approach, attribution method, and data quality considerations. Below is a clear, brief overview of all ten:

1. Listed Equity and Corporate Bonds

This covers shares and bonds of publicly traded companies held for general corporate purposes. Emissions are attributed using the financial institution’s share of the company’s enterprise value (usually EVIC — Enterprise Value Including Cash). It benefits from better data availability through company disclosures.

2. Business Loans and Unlisted Equity

This includes loans and equity investments in private companies, SMEs, and nonprofits. Attribution is typically based on the outstanding loan amount or equity share relative to the borrower’s total assets or equity. Data often relies on a mix of client-reported information and sector benchmarks.

3. Project Finance

This asset class covers loans or equity for specific, ring-fenced projects such as power plants, infrastructure, or renewable energy developments. Because the use of proceeds is known, emissions can be calculated more accurately at the project level rather than the corporate level.

4. Commercial Real Estate

This includes loans and investments in income-producing commercial properties like offices, retail spaces, hotels, and industrial buildings. Calculations use building-specific energy use, floor area, or occupancy data along with location-based emission factors.

5. Mortgages

This covers residential home loans for purchase or refinancing. Emissions are estimated using property type, location, energy performance certificates (where available), and location-specific emission factors.

6. Motor Vehicle Loans

This includes loans for passenger vehicles, commercial fleets, and other motor vehicles. Calculations are based on vehicle type, fuel efficiency, mileage data, and expected lifetime emissions.

7. Sovereign Debt

This asset class covers government bonds and loans to national governments. Emissions are attributed based on the financial institution’s share of a country’s total outstanding debt, using national greenhouse gas inventory data.

8. Sub-sovereign Debt

This includes bonds and loans issued by state, provincial, municipal, or local governments. It uses similar attribution logic as sovereign debt but at a more granular regional or city level, which is particularly relevant for infrastructure and urban development financing.

9. Use-of-Proceeds Structures

This covers instruments where the funds are earmarked for specific purposes, such as green bonds, sustainability-linked bonds/loans, and dedicated funds. Emissions accounting focuses on the underlying assets or projects being financed rather than the issuer’s overall emissions.

10. Securitisations and Structured Products

This includes asset-backed securities such as RMBS, CMBS, CLOs, and other structured finance products. The methodology looks through to the underlying collateral (e.g., mortgages, auto loans, or corporate loans) and applies the relevant asset-class methodology to those underlying exposures.

Each asset class introduces its own data‑quality challenges, from full corporate‑level disclosure for listed equity to heavy reliance on proxies for mortgages and SME loans.

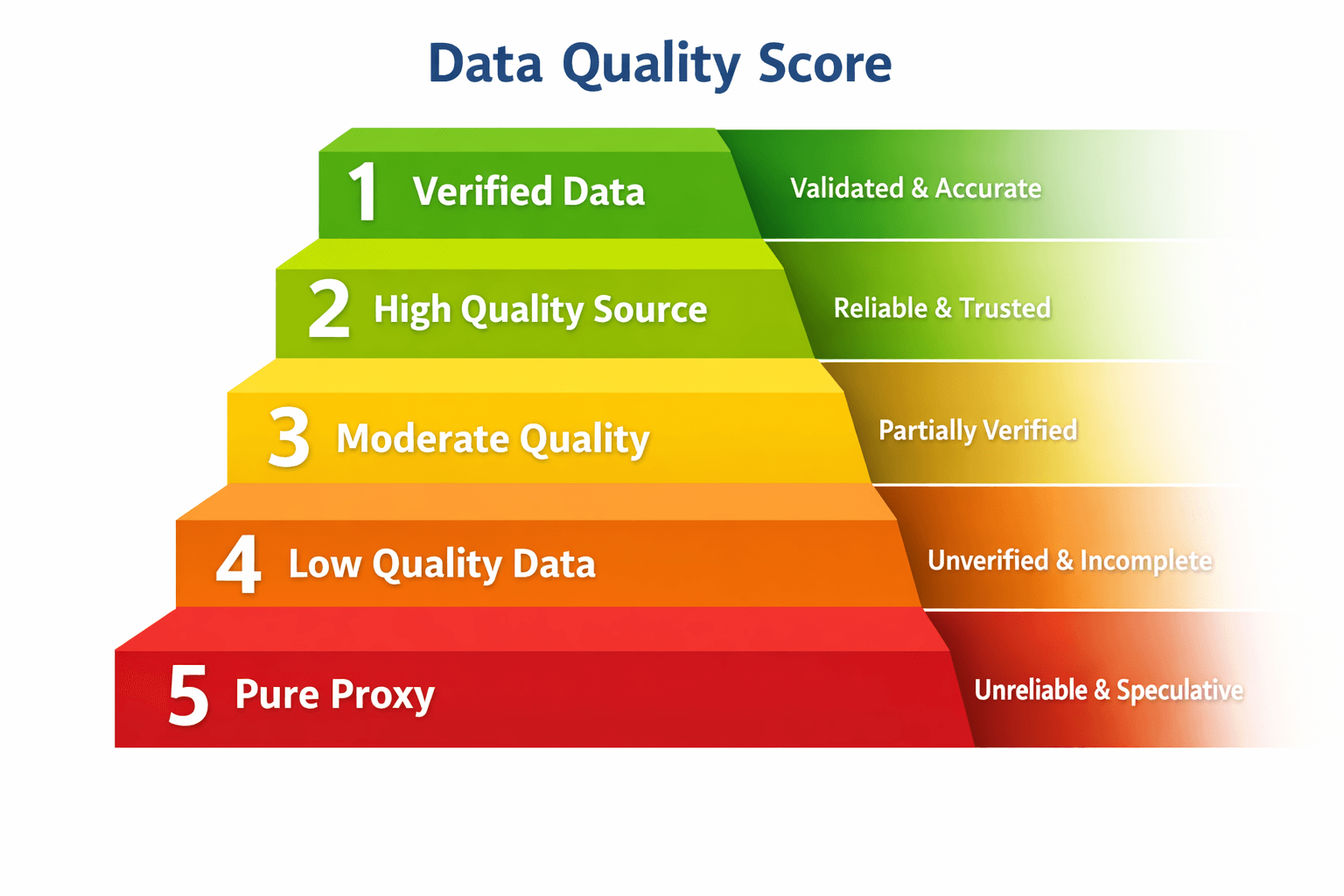

Understanding the data‑quality score

PCAF introduced a five‑tier data‑quality scoreto help institutions signal how reliable their financed‑emissions estimates are, on a scale from 1 (highest quality) to 5 (lowest quality). The score is assigned per asset‑class exposure, reflecting the source and method used to calculate emissions rather than the absolute emissions number itself.

- Score 1 – Verified, direct emissions data

The investee provides verified Scope 1 and 2 emissions; the financial institution uses these directly, with a PCAF‑aligned attribution factor and no meaningful estimation. - Score 2 – Non‑verified, direct emissions data

The investee reports emissions that are not independently verified, but the data is still primary and specific to that company or asset. - Score 3 – Activity‑based estimates with good proxies

No direct emissions data is available, so the institution uses detailed activity data (e.g., energy consumption, fuel use) combined with sector‑specific emission factors to estimate emissions. - Score 4 – Company‑level estimates with limited activity data

Limited activity data is available; the institution relies on higher‑level financial or sector‑level proxies, introducing more uncertainty. - Score 5 – Pure proxy‑based estimates

The institution uses only high‑level proxies such as revenue‑ or spend‑based multipliers, with no granular activity or asset‑level data; this is the weakest quality tier.

A typical bank or asset manager today may have large portions of its portfolio sitting at scores 4 or 5, especially for SMEs, private equity, real estate, and consumer‑facing loans, where investor‑level disclosures are sparse.

Why data‑quality matters for financed emissions

High‑quality data is not just about “cleaner” numbers; it directly shapes the credibility of your climate‑risk narrative, your transition‑planning assumptions, and your ability to engage with regulators and investors. Regulators and investors increasingly expect not only a financed‑emissions total, but also a breakdown of data‑quality scores by asset class, so they can see how much of your footprint is based on proxies versus actual measurement.

Moving from score 5 or 4 to score 3 or 2 is a practical and meaningful ambition for most institutions. It means:

- Replacing generic revenue‑based proxies with activity‑based drivers(energy, fuel, building‑type, vehicle type, etc.).

- Integrating sector‑specific emission factorsand PCAF‑aligned benchmarks where company‑level data is missing.

- Systematically tracking and improving coverage and traceability of emissions data across the portfolio.

This is where a structured, PCAF‑aligned software platform becomes essential, not to hide the process, but to illuminate it.

How EnDecarb.ai helps improve your data‑quality score

EnDecarb.ai is built around the PCAF financed emissions framework, helping banks, asset managers, and other financial institutions move from fragmented, low‑quality estimates to a more robust, transparent, and auditable financed emissions inventory. The platform supports institutions in shifting exposures from score 5 to score 3 or 2 by bringing data, calculations, and quality tracking into one integrated environment.

Asset class specific calculation engines

For each PCAF asset class such as listed equity, corporate bonds, business loans, project finance, commercial real estate, mortgages, and motor vehicle loans, EnDecarb.ai applies the correct PCAF methodology, including attribution factors and data quality rules. This keeps calculations consistent, standards aligned, and easier to defend in front of auditors and regulators.

Data quality score tracking at exposure level

The platform automatically assigns and tracks a data quality score from 1 to 5 for every loan, holding, or project. This makes it easy to see where the portfolio relies on high level proxies and where better quality data already exists, so teams can focus data collection on the most material exposures.

Stepping from proxy to activity based

EnDecarb.ai helps organisations systematically move from pure proxy estimates at score 5 toward activity based or company level estimates at scores 3 or 2. This can include integrating utility, energy, and building performance data, using sector specific emission factors and benchmarks, and running structured data collection campaigns with borrowers and investors so that more exposures gradually move into higher quality bands.

No black box approach

Unlike opaque tools that are treated as black boxes, EnDecarb.ai makes methodologies, assumptions, and data sources visible and traceable. Every emission number, quality score, and attribution factor can be traced back to its origin, which simplifies internal audits, external assurance, and dialogue with regulators and investors.

Clear reporting for stakeholders

The platform supports clear, PCAF aligned reporting and dashboards that show financed emissions by asset class, sector, and data quality band. This helps institutions demonstrate a visible progression from low quality proxies toward higher quality, activity based measurement, in a way that aligns with the expectations seen in TCFD, ISSB, and SFDR style disclosures.

A first for EnDecarb.ai: PCAF accreditation

EnDecarb.ai is proud to be the first software platform headquartered in India to receive accreditation as a Regional Accredited Partner from the Partnership for Carbon Accounting Financials (PCAF). This accreditation confirms that our platform’s methodologies for financed emissions calculation, data quality scoring, and reporting fully align with the latest PCAF Global GHG Accounting and Reporting Standard. It provides our clients with confidence that their financed emissions calculations are transparent, auditable, and compliant with international best practices.

For financial institutions, this accreditation:

- Reduces implementation risk by ensuring that your software layer is already aligned with PCAF requirements.

- Builds confidencewith regulators, auditors, and investors that your financed‑emissions data is built on a recognised, standards‑based foundation.

Turning financed emissions into a strategic advantage

Treating financed emissions as a one‑off compliance exercise leads to frustration and poor outcomes. Done right, they become a strategic lever to understand climate risk at the portfolio level, shape lending and investment policy, and engage borrowers and investors in decarbonisation.

By combining rigorous treatment of PCAF asset classes, a deliberate focus on data quality scores 1–5, and a transparent, PCAF‑aligned platform like EnDecarb.ai, institutions can move from guessing to governing their financed emissions footprint.

If you lead climate risk, ESG, or sustainability reporting at a bank, asset manager, or insurer, EnDecarb.ai helps you spend less time on spreadsheets and more time shaping a credible, finance aligned net‑zero pathway for your portfolio and stakeholders.