GHG accounting is the discipline of measuring your organisation’s greenhouse gas emissions across all sources — direct, indirect, and through your value chain or lending portfolio. In 2026, it is no longer optional. BRSR Core mandates Scope 1 and 2 disclosure with reasonable assurance for India’s top listed companies. Banks face financed emissions requirements under PCAF. Scope 3 — including net zero pathways and decarbonisation planning — is where most real emissions and most real climate risk actually live. This guide explains how it all works, where organisations go wrong, and how to build a credible programme that serves both compliance and strategy.

The Question That Reveals Where Most Organisations Stand

Here is a question that most sustainability teams cannot answer cleanly: if your organisation shut down tomorrow and stopped all its operations, what percentage of your total greenhouse gas footprint would actually disappear?

For most manufacturers: less than 30% of total GHG footprint comes from direct operations.

For most banks: less than 1% — the rest sits in the loan book.

That is the central insight of GHG accounting — the systematic measurement of where your emissions actually come from, across your own operations and everything connected to them. And it is why getting GHG accounting right has become one of the more consequential things an organisation can do in 2026.

This guide explains what GHG accounting is, how the three scopes work in practice, what the standards require, where organisations consistently go wrong, and what the current landscape looks like for Indian companies and financial institutions — including the net zero and decarbonisation implications that make this more than a reporting exercise.

What GHG Accounting Actually Means

GHG accounting is the process of creating a structured, verifiable inventory of the greenhouse gases your organisation releases into the atmosphere — directly and indirectly. It follows the same discipline as financial accounting: defined boundaries, consistent methodology, traceable data, and third-party verification. The difference is that instead of tracking cash flows, you are tracking emissions of carbon dioxide, methane, nitrous oxide, and several other gases, all expressed in a common unit called CO₂ equivalent (CO₂e).

The CO₂ equivalent conversion matters because different gases trap heat at different intensities. Methane is roughly 28 times more potent than CO₂ over a 100-year period. Nitrous oxide is approximately 273 times more potent. The gases covered are:

- Carbon dioxide (CO₂) — from fuel combustion and industrial processes

- Methane (CH₄) — from agriculture, waste decomposition, and natural gas systems

- Nitrous oxide (N₂O) — from fertiliser application and certain industrial processes

- Hydrofluorocarbons (HFCs) — from refrigerants and air conditioning systems

- Perfluorocarbons (PFCs) — from aluminium production and semiconductor manufacturing

- Sulphur hexafluoride (SF₆) — from high-voltage electrical transmission equipment

- Nitrogen trifluoride (NF₃) — from electronics and solar panel manufacturing

What GHG accounting is not is a sustainability report. The report is the output. The accounting is the underlying process — data collection, emission factor application, calculation, and documentation. Organisations that treat GHG reporting as a communications exercise and work backwards from the number they want to disclose are not doing GHG accounting. They are doing something else, and experienced auditors and investors can tell the difference immediately.

The Three Scopes — Where Your Emissions Actually Come From

The Greenhouse Gas Protocol — the global standard developed by the World Resources Institute and the World Business Council for Sustainable Development — organises emissions into three scopes. This structure exists for one practical reason: to avoid double-counting while ensuring a complete picture of organisational impact.

SCOPE 1

Direct Emissions

- • Fuel combustion

- • Company vehicles

- • On-site processes

- • Refrigerant leaks

SCOPE 2

Indirect Energy

- • Grid electricity

- • Purchased steam

- • District cooling

- • Heat from utilities

SCOPE 3

Value Chain (15 categories)

- • Supply chain (Cat 1-8)

- • Business travel

- • Employee commute

- • Financed emissions (Cat 15)

| Scope | Type | Examples | Measurement Difficulty |

|---|---|---|---|

| Scope 1 | Direct — owned sources | Diesel generators, company vehicles, refrigerants, on-site boilers | Low — data is internal |

| Scope 2 | Indirect — purchased energy | Grid electricity, purchased steam, heat, and cooling | Low-Medium — CEA factors available; requires both location and market-based calc. |

| Scope 3 | Value chain — 15 categories | Supply chain, business travel, employee commute, financed emissions (Cat 15) | High — requires supplier, partner, and borrower data |

Scope 1 — Your Direct Footprint

Scope 1 captures emissions from sources you own or control. Diesel in your generator. Petrol in your company fleet. Natural gas in your boiler. Refrigerant leaking from your air conditioning systems. For a cement plant or a steel mill, Scope 1 is the dominant emission source. For a bank or an IT company, it is usually small — but never negligible.

Scope 1 is the most straightforward to measure because the data is internal. The challenge is completeness — are you capturing every emission source? — and consistency — are you using the same methodology year on year so your trends are meaningful rather than artefacts of methodological change?

Scope 2 — Your Electricity Footprint

Scope 2 covers the emissions from generating the energy you purchase and consume — principally grid electricity. The combustion happens at the power station, not at your facility. But you created the demand, so the emissions are attributed to you.

In India, Scope 2 from purchased electricity is calculated using the CEA grid emission factor, published annually by the Central Electricity Authority. Due to India’s rapid expansion of solar and wind capacity, this figure has been falling and now typically ranges between 0.70 and 0.82 tCO₂ per MWh depending on the year and regional grid. Always use the most recent CEA annual report for your reporting period and check whether a national or regional factor is more appropriate for your facility locations.

The GHG Protocol requires two reporting approaches. The location-based method uses this average grid factor. The market-based method uses supplier-specific factors from renewable energy certificates or power purchase agreements. Both must be reported where possible — not chosen between.

Scope 3 — Where Most of the Emissions Actually Live

Scope 3 is every other indirect emission across your value chain, organised into 15 categories. According to CDP data, Scope 3 accounts for more than 70 percent of total emissions across most industry sectors. In financial services, food, and fashion, it frequently exceeds 90 percent.

The 15 categories span both upstream activities — what happens before goods and services reach you — and downstream activities — what happens after you have provided them:

- Category 1: Purchased goods and services

- Category 2: Capital goods

- Category 3: Fuel and energy related activities (upstream, not in Scope 1 or 2)

- Category 4: Upstream transportation and distribution

- Category 5: Waste generated in operations

- Category 6: Business travel

- Category 7: Employee commuting

- Category 8: Upstream leased assets

- Category 9: Downstream transportation and distribution

- Category 10: Processing of sold products

- Category 11: Use of sold products

- Category 12: End-of-life treatment of sold products

- Category 13: Downstream leased assets

- Category 14: Franchises

- Category 15: Investments — financed emissions

A note on Category 3 — What Scope 2 Does Not Capture

Category 3 is widely misunderstood and consistently underreported. It covers the upstream emissions that are not counted in Scope 1 or Scope 2 but are directly caused by your energy use. This includes three things: the extraction and refining of fuels you burn (well-to-tank emissions above and beyond the combustion you report in Scope 1), the extraction of fuels used to generate the electricity you consume (the upstream layer above your Scope 2 number), and — critically for India — transmission and distribution losses.

Category 15 — Why It Rewrites the Conversation for Banks

For banks, NBFCs, and insurers, Category 15 is not one line in a table. It is the entire story. A mid-sized Indian bank might have a combined Scope 1 and 2 footprint of 50,000 to 80,000 tonnes CO₂e from its offices, branches, data centres, and fleet. That is not a trivial number. But it is almost certainly less than one percent of the bank’s actual climate exposure.

The other 99 percent sits in financed emissions — the GHG emissions associated with its loans, bonds, equity investments, and underwriting activities. A bank lending to steel plants, coal-based power generators, cement manufacturers, and real estate developers is financing tens of millions of tonnes of CO₂e annually. Those emissions appear in no one’s Scope 1. They sit in the bank’s Scope 3 Category 15.

The Partnership for Carbon Accounting Financials — PCAF — provides the globally recognised methodology for calculating financed emissions. It covers all major asset classes: listed equity and corporate bonds, business loans and unlisted equity, project finance, commercial real estate, mortgages, and motor vehicle loans. Each uses a data quality score from 1 (precise, borrower-specific data) to 5 (least precise, sector-level proxy).

The Standards and Frameworks You Need to Know

The GHG Protocol — The Foundation

The GHG Protocol Corporate Standard remains the global foundation for organisational-level GHG accounting. Every major framework — BRSR, ISSB, TCFD, SBTi, PCAF — builds on or explicitly references GHG Protocol definitions, scope boundaries, and methodologies.

BRSR — India’s Mandatory Disclosure Framework

The Business Responsibility and Sustainability Reporting framework, mandated by SEBI, is the central regulatory instrument for GHG disclosure among India’s listed companies. BRSR Core — the assurance-backed subset — requires disclosure of Scope 1 and Scope 2 GHG emissions with reasonable assurance.

| Disclosure | Scope Coverage | Assurance Level | Who it applies to |

|---|---|---|---|

| BRSR Core — GHG disclosures | Scope 1 & 2 (mandatory) | Reasonable assurance | Top listed companies per SEBI glide path (expanding annually) |

| BRSR Extended — value chain | Scope 3 (encouraged) | Limited assurance | Top 1,000 listed companies |

| Energy intensity metrics | Scope 1 & 2 derived | Included in Core assurance | Per SEBI glide path |

| PCAF-aligned financed emissions (RBI framework, forthcoming) | Scope 3 Category 15 | External methodology accreditation | Banks, NBFCs, insurers |

SBTi — Tightening the Net Zero Pathway Requirements

The Science Based Targets initiative validates corporate climate targets against 1.5°C-aligned pathways. In 2025 and 2026, SBTi significantly tightened its Scope 3 rules. Companies in certain sectors can no longer have their targets validated without a credible Scope 3 accounting base. SBTi also updated its financial institution framework, requiring banks and investors to set portfolio-level emission targets that must be grounded in PCAF-aligned financed emissions data.

PCAF — The Financial Sector Methodology

PCAF is the required methodology for any financial institution calculating financed emissions credibly. PCAF accreditation — where a software provider or methodology is independently reviewed against PCAF’s requirements — is increasingly being used by banks as a selection criterion for GHG accounting partners.

ISSB and IFRS S2 — The International Reference Point

The International Sustainability Standards Board’s IFRS S2 Climate-related Disclosures requires companies to disclose climate risks, opportunities, and GHG emissions across all three scopes. Not yet mandatory in India, but already the reference standard for Indian companies with international listings, foreign institutional investors, or global supply chain relationships.

Five Things Organisations Consistently Get Wrong

1. Starting before the foundations are solid

The most common mistake is attempting Scope 3 before Scope 1 and 2 are properly established. The correct sequence is: lock your boundary, get Scope 1 right, get Scope 2 right using both methods, then build Scope 3 category by category, starting with material ones.

2. Using the wrong emission factors — or the right ones in the wrong place

Using an outdated CEA grid factor, applying a national factor when regional disaggregation is available, or using combustion-only IPCC defaults where a well-to-tank factor is needed — these are systematic errors that compound year on year.

3. Inconsistent organisational boundaries

The GHG Protocol allows three approaches: equity share, financial control, and operational control. Many organisations inadvertently mix these without realising that this makes year-on-year comparability unreliable. Define your approach, document it explicitly, and apply it consistently.

4. No audit trail

A GHG inventory that cannot be audited is not an inventory — it is a claim. Every number needs to be traceable from the final disclosure back to the raw activity data, through the emission factor applied, to the source and version of that factor.

5. Treating it as a compliance exercise rather than a strategic tool

GHG data that is collected, calculated, disclosed, and then filed away generates no business value. The same inventory that feeds your BRSR disclosure should be informing your capital allocation, your supplier engagement strategy, and your transition planning.

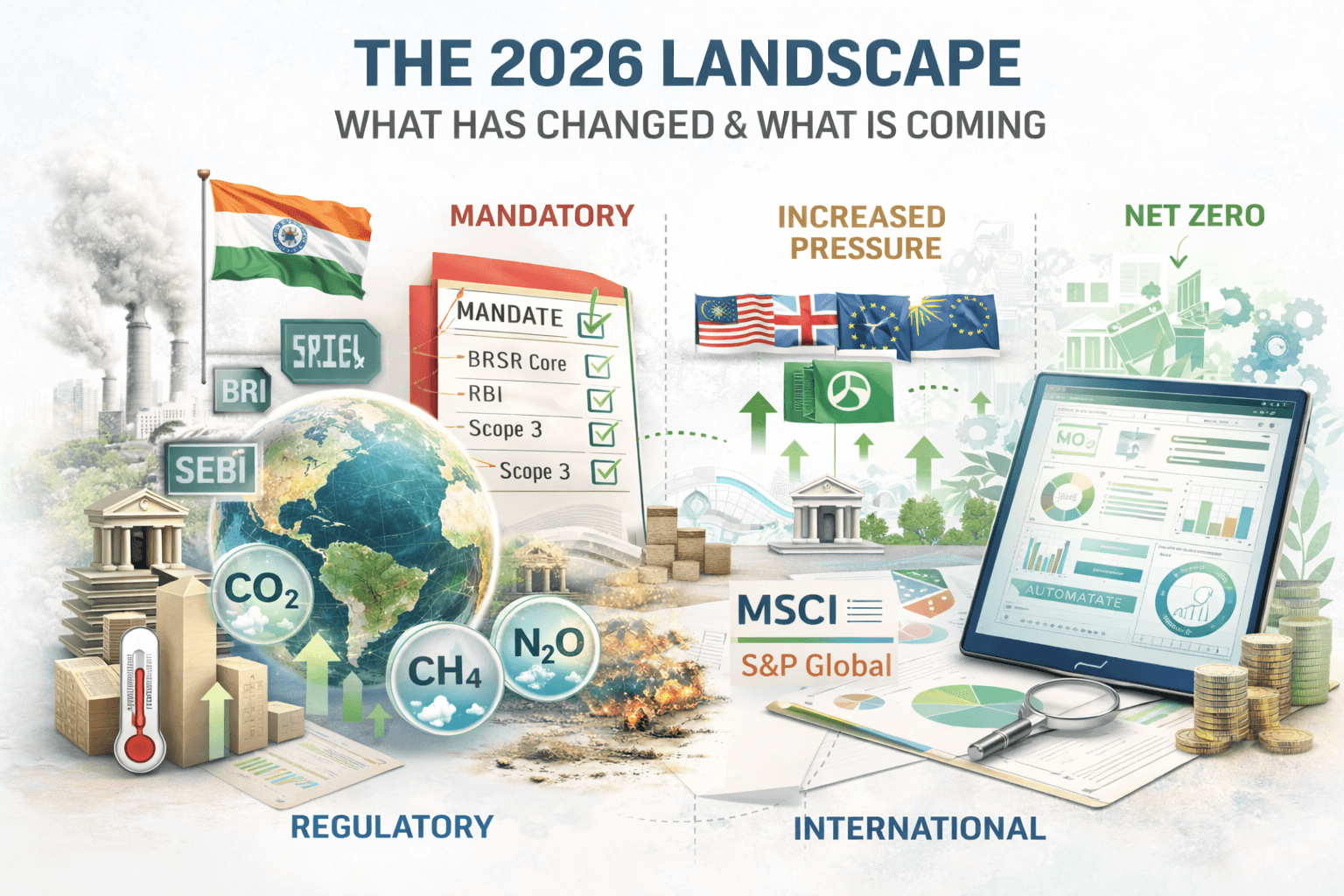

The 2026 Landscape — What Has Changed and What Is Coming

Indian regulatory requirements have shifted from guidance to mandate

BRSR Core with reasonable assurance is active and expanding. The RBI draft climate disclosure framework is in its final stages. For financial institutions, the convergence of BRSR, RBI guidelines, and PCAF requirements means the regulatory ask is operational, not theoretical.

International capital is applying pressure from the top

Foreign portfolio investors, sovereign wealth funds, and development finance institutions evaluating Indian companies and banks are asking for TCFD-aligned disclosures and PCAF-aligned financed emissions data as a condition of capital.

Net zero commitments require the accounting infrastructure to back them

A net zero commitment without a credible emissions baseline is a communications statement, not a strategy. SBTi's tightened validation rules, investor due diligence standards, and emerging regulatory requirements are converging on the same point.

Technology has changed what is feasible

GHG accounting used to require months of manual data collection. Modern platforms now automate data ingestion, apply correct emission factors, calculate financed emissions under PCAF rules, generate audit-ready outputs, and produce disclosure-formatted reports aligned with BRSR, TCFD, and IFRS S2.

Eight Steps to a Credible GHG Accounting Programme

There is no shortcut to a credible GHG inventory, but there is a clear sequence that applies whether you are a manufacturer, an IT company, a conglomerate, or a bank.

Define your organisational boundary. Choose equity share, financial control, or operational control. Document the choice explicitly. Apply it to every entity, joint venture, and subsidiary. Define the conditions under which you will restate.

Set your base year. Pick a recent year with reliable data. Document the restating policy before you need it. A base year that keeps shifting makes trend analysis meaningless.

Collect Scope 1 activity data. Fuel purchase records, generator consumption logs, refrigerant top-up quantities, industrial process records. Build data collection into operational systems, not as an annual scramble.

Collect Scope 2 activity data. Electricity bills for every metered location. Map each location to the correct regional grid factor using the current CEA annual report. Calculate both location-based and market-based figures.

Prioritise and collect Scope 3 data. Run a screening exercise to identify which categories are material for your sector. For most Indian manufacturers: Categories 1, 3, 4, and 11. For banks: Category 15 is the entire story.

Apply correct emission factors. CEA grid factors (current year) for Scope 2. IPCC or national defaults for fuel combustion. DEFRA conversion factors for upstream and lifecycle Scope 3 categories. PCAF methodology for financed emissions.

Build the audit trail from day one. Every calculation traceable from output to raw data to emission factor to source. Not retrofitted — built in. This is what reasonable assurance requires.

Obtain third-party assurance. Reasonable assurance is mandatory for BRSR Core. Plan for assurance from the start. Use the data to drive decarbonisation decisions, not just to meet a disclosure deadline.

How EnDecarb.ai Makes GHG Accounting Accurate, Transparent, and Actionable

GHG accounting at the level of quality the 2026 regulatory and investor landscape demands is not a spreadsheet problem. It is a data infrastructure problem. And for financial institutions, it is also a methodology problem — PCAF-aligned financed emissions calculation across multiple asset classes, for thousands of counterparties, with data quality scoring and audit-ready outputs, cannot be done at scale without purpose-built infrastructure.

EnDecarb.ai is an AI-powered GHG accounting and climate risk platform built for Indian enterprises and financial institutions, aligned with the standards that matter in 2026.

For enterprises — manufacturers, IT companies, conglomerates

- Scope 1, 2, and 3 in a single platform. Automated data ingestion from your ERP, utility bills, and procurement systems. Correct emission factors applied by source and category.

- BRSR reporting built in. BRSR Core disclosure outputs in the required format, with full methodology documentation. Designed to survive reasonable assurance from day one.

- Decarbonisation pathway support. The platform connects your emissions inventory directly to decarbonisation scenario modelling.

- Full audit trail at every step. Every calculation traceable from disclosure back to raw activity data. No black boxes.

For banks, NBFCs, and insurers

- PCAF-accredited financed emissions. EnDecarb.ai is the first PCAF-accredited software and methodology provider in South Asia, covering all PCAF asset classes with data quality scoring at the counterparty level.

- RBI draft disclosure alignment. The platform is built around the RBI draft climate disclosure framework.

- Physical and transition risk integration. Financed emissions data connects directly to physical risk heat maps, NGFS Phase IV transition scenarios, and climate stress testing.

- Portfolio-level net zero pathway modelling. Understand how your current portfolio composition maps against net zero targets.

- Peer benchmarking. Compare your portfolio emissions intensity against Indian and international peers using disclosed BRSR, TCFD, and CDP data.

Frequently Asked Questions

Is GHG accounting mandatory for Indian companies?

Yes, partially, and the scope is expanding. BRSR Core requires Scope 1 and 2 disclosure with reasonable assurance for the top listed companies per the SEBI glide path. Full BRSR disclosures are required for the top 1,000 listed companies. For banks, the RBI draft climate disclosure framework will create mandatory requirements when finalised.

What is the difference between Scope 2 and Scope 3 Category 3?

Scope 2 covers the combustion emissions at the power station generating the electricity you consume. Scope 3 Category 3 captures what Scope 2 misses: the upstream extraction and processing of fuels used to generate that electricity, plus transmission and distribution losses. In India, T&D losses are higher than the global average, making Category 3 more material.

What emission factors should Indian companies use for each scope?

Scope 2 location-based: current year CEA CO₂ Baseline Database (typically 0.70–0.82 tCO₂/MWh). Scope 1 fuel combustion: IPCC defaults or national fuel-specific factors. Scope 3 upstream categories: DEFRA conversion factors. Financed emissions: PCAF-approved sector emission intensity data.

What does PCAF accreditation mean for a software provider?

PCAF accreditation means the software provider's methodology has been independently reviewed by PCAF's technical team and confirmed to meet the requirements of the PCAF Standard for financed emissions calculation. It is equivalent to a methodology audit — not a self-declaration.

How does GHG accounting connect to net zero and decarbonisation strategy?

A credible net zero pathway requires a reliable baseline, an understanding of where the largest reduction opportunities lie, and a monitoring mechanism to track progress. GHG accounting provides all three. Without it, a net zero commitment is a target without a plan.

How long does it take to build a GHG inventory?

With the right platform and data access, Scope 1 and 2 for a single entity can be completed in weeks. A multi-entity Scope 1, 2, and material Scope 3 inventory — assurance-ready — typically takes two to three months in the first year. For banks, a financed emissions pilot typically takes four to eight weeks.

The Bottom Line

GHG accounting is not about meeting a reporting deadline. It is about understanding the real emissions profile of your organisation, your supply chain, and your portfolio — and using that understanding to make better decisions about risk, capital, strategy, and your net zero pathway.

The organisations that build this capability now — with the right methodology, data infrastructure, and genuine transparency — will have a material advantage as the regulatory and investor landscape continues to tighten. The ones waiting for the mandate will find they are starting a year behind.

www.endecarb.ai | The Climate Ledger Newsletter | endecarbnewsletter.substack.com